Introduction: The Weaver’s Loom of the 21st Century

In the early nineteenth century, the city of Lowell, Massachusetts, became the cradle of the American Industrial Revolution by introducing a radical concept: the integrated textile mill. Before Lowell, the manufacturing of cloth was a fractured, modular affair. One merchant bought raw cotton; another cleaned it; a separate cottage spinner spun it into yarn; a distant weaver turned it into fabric; and a final finishing shop dyed, pressed, and packaged the cloth. Each participant optimized his own narrow step, traded with the others across open markets, and remained blissfully indifferent to what happened upstream or downstream of his own workbench.

Francis Cabot Lowell changed everything by bringing all of these disparate steps under a single roof, driven by a unified waterwheel. Under one industrial system, raw cotton entered at the ground floor, and finished, pristine fabric exited from the top. It was not merely an optimization of labor; it was a total collapse of a fragmented supply chain into a single, breathing entity. The economics of the mill were not the economics of spinning plus the economics of weaving plus the economics of dyeing. They were the economics of the whole — of the river’s flow rate, the waterwheel’s torque, the belt-drive’s losses, and the synchronized cadence of every machine on every floor. To analyze a Lowell mill by studying a single thread of cotton was to miss the entire point of the institution.

Today, the frontier artificial intelligence laboratory is undergoing an identical transformation. For the past decade, Silicon Valley operated on the myth of clean, modular separation. Algorithms were written by research scientists; chips were bought from merchant vendors; compute was rented by the hour from standardized clouds; and power was pulled quietly and anonymously from the wall. That software-centric era is dead. In its place has arisen something that looks far more like Lowell’s Massachusetts than like the garage-startup mythology of Palo Alto: a capital-devouring, energy-hungry, physically enormous industrial complex whose combined 2026 construction budget — roughly $725 billion across Alphabet, Amazon, Meta, and Microsoft alone, up 77 percent from the record $410 billion spent in 2025 — already rivals the inflation-adjusted cost of the entire U.S. Interstate Highway System, compressed into a single year.[1][2]

We have entered the era of the Five-Layer AI Economy. The modern frontier AI lab can no longer survive as a pure software play. To train the next generation of models, a lab must fundamentally transform. It must simultaneously act as an energy buyer negotiating gigawatt-scale nuclear contracts, a semiconductor customer co-designing proprietary silicon with the world’s most advanced foundries, a cloud tenant orchestrating hyper-scale optical fabrics, and an infrastructure planner mapping out planetary logistics of land, water, concrete, and copper. Amazon’s $11 billion Project Rainier campus in Indiana — built on former cornfields, dedicated to a single customer, and running more than one million custom Trainium chips — is not a metaphor for this transformation; it is the transformation itself, poured in concrete.[8][9]

This paper argues that the five layers of the AI economy — energy, chips, datacenters, models, and applications — are no longer distinct industries interacting through an open market. They have permanently fused. The silicon, the data center, the power grid, and the neural network have collapsed into a single, vertically integrated machine. We title this work “One Industrial System” because, much like Lowell’s historic mill, one can no longer analyze the code without analyzing the power plant that generates the tokens. They are integrated components of the exact same industrial loom, spinning the fabric of twenty-first-century synthetic intelligence.

The argument proceeds in six sections. Section 1 establishes the theoretical shift from software-centric to infrastructure-determinist AI, grounding it in the empirical scaling laws that govern model capability. Section 2 surveys the modern hardware landscape as it stands in mid-2026 — Nvidia’s platformization, the hyperscaler custom-silicon counter-offensive, and the megaproject era of gigawatt-scale clusters. Section 3 formalizes the Five-Layer AI Economy and demonstrates why the modular stack has collapsed into an interdependency trap that forces a four-fold corporate identity. Section 4 traces the macro implications: the sovereign AI race, the weaponization of export controls, and the existential squeeze on startups. Section 5 weighs the double-edged sword of vertical integration — systemic resilience against monopoly risk — drawing on the warnings of leading academic economists. Section 6 distills the analysis into seven strategic pillars, and the Conclusion returns to Lowell’s loom to ask what kind of civilization builds its intelligence this way.

Section 1: The Infrastructure Determinism of Frontier AI

For the first seven decades of its history, computer science operated on a fundamental assumption: software was an ethereal layer of logic, gracefully insulated from the messy, material realities of the hardware beneath it. In Silicon Valley, this assumption hardened into a dominant cultural myth. Brilliance was measured in algorithmic elegance, loss functions, and architectural tweaks written in clean code. The physical machine was viewed as a commoditized utility — a generic basin of compute to be rented by the hour from a standard cloud provider. Venture capitalists priced this myth into their portfolios: software companies deserved software multiples precisely because they were unburdened by factories, inventories, supply chains, or utility bills. The entire intellectual apparatus of the industry, from “agile development” to “serverless architecture,” was constructed on the premise that atoms had been successfully abstracted away.

This software-centric paradigm is officially dead. The relentless progression of frontier artificial intelligence has collided with the hard boundaries of physical scaling laws, triggering an abrupt transition into an era of deep infrastructure determinism. Algorithmic refinements have not lost their value — indeed, mixture-of-experts routing, speculative decoding, and reinforcement-learning-based reasoning have delivered enormous efficiency gains — but their efficacy is now entirely bound to, and constrained by, the massive industrial footprint that hosts them. The defining question of a frontier lab’s roadmap is no longer “what architecture should we try next?” but “how many megawatts can we energize by which quarter, and how much high-bandwidth memory have we contractually secured?”

The intellectual origin of this shift can be dated with unusual precision. In 2020, Jared Kaplan, Sam McCandlish, and colleagues published “Scaling Laws for Neural Language Models,” demonstrating that model loss declines as a smooth, predictable power-law function of three inputs: parameters, data, and total training compute measured in floating-point operations.[56] The paper’s implication was profound and, in retrospect, civilizational: intelligence had acquired a manufacturing function. Capability was no longer the unpredictable output of scientific genius; it was the predictable output of industrial throughput. Once capability became a function of FLOPs, and FLOPs became a function of chips, power, cooling, and interconnect, the destiny of AI passed out of the hands of algorithm designers and into the hands of those who could marshal land, concrete, water, copper, silicon, and raw electrical current at planetary scale. The Stanford Institute for Human-Centered AI’s 2026 AI Index confirms that the industrial logic has, if anything, accelerated: training compute for notable frontier models has grown roughly 3.3 times per year since 2022, over 90 percent of notable models now originate inside private companies rather than academia, and the entire hardware supply chain funnels through a startlingly narrow set of physical chokepoints.[28][29]

The economists saw the pattern before most technologists admitted it. Erik Brynjolfsson, director of the Stanford Digital Economy Lab, has long classified AI as the most consequential member of a rare category of innovations:

“AI is what I call a general-purpose technology.”

— Erik Brynjolfsson, Stanford Digital Economy Lab [33]

Brynjolfsson’s comparison set — the steam engine, electricity — is instructive precisely because those technologies were not adopted as products but as infrastructures. Electricity did not change the world when the first dynamo spun; it changed the world when factories were physically rebuilt around electric drive, when grids were strung across continents, and when a half-century of complementary capital investment restructured the entire economy around the new energy form.[33] Frontier AI is now recapitulating that pattern at compressed speed, and the complementary capital investment is arriving not over fifty years but over five: the International Monetary Fund’s 2026 analyses find that AI-related technology investment has become powerful enough to shape national growth surprises, with the top net exporters of AI hardware posting a 4.4-percentage-point average first-quarter 2026 growth surprise while the rest of the world was flat, even as the Fund cautions that a reevaluation of AI profit expectations could trigger an abrupt financial correction.[34][35]

The paradigm shift can be summarized in a single comparative frame. In the software-centric past, progress was gated by ideas and talent; in the infrastructure-determinist present, progress is gated by physics, permits, and purchase agreements. In the past, the constraint was the imagination of a research team; in the present, the constraint is the interconnection queue of a regional transmission organization and the wafer allocation schedule of a single Taiwanese foundry. In the past, an AI lab’s balance sheet looked like a media company’s; in the present, it looks like a railroad’s.

| Dimension | Past: Software-Centric Era | Future: Infrastructure-Determinist Era |

| Primary driver of progress | Pure algorithmic tweaks; architectural elegance | Physical scaling laws; total FLOPs throughput[56] |

| Compute posture | Commoditized cloud rental by the hour | Heavy capital lock-in; owned gigawatt campuses[8][12] |

| Organizational form | Isolated research labs; small teams | Integrated energy-silicon-datacenter conglomerates[26] |

| Binding constraint | Talent and ideas | Grid interconnection, HBM supply, foundry allocation[22][44][48] |

| Financial profile | Asset-light; software multiples | Asset-heavy; $725B combined 2026 hyperscaler capex[1][2] |

| Failure mode | Product-market fit miss | Stranded gigawatts; correlated capex re-rating[55] |

Table 1. The paradigm shift in AI progress: from software-centric to infrastructure-determinist development.

To contextualize this transformation, this paper looks back to the birth of modern manufacturing: Francis Cabot Lowell’s integrated textile mill in nineteenth-century Massachusetts. Before Lowell, textile production was a highly fractured, horizontal affair scattered across independent cottage spinners, weavers, and dyers. Lowell’s genius was not a change in the mechanics of spinning yarn, but a radical consolidation of the entire supply chain. By bringing every disparate step under a single roof driven by a unified waterwheel, he created a singular, continuous machine where raw cotton entered the ground floor and finished fabric emerged from the top. The waterwheel — the energy layer — was not an accessory to the mill; it was the mill’s beating heart, and every machine above it was designed around its rhythm.

Today, the Five-Layer AI Economy demands an identical collapse of the technology stack. The traditional walls separating basal energy, custom semiconductor design, hyper-scale cloud fabrics, foundational models, and consumer applications are actively dissolving. A modern frontier AI lab cannot survive as a pure software play; it must simultaneously operate as an energy buyer securing gigawatt-scale grid allocations and nuclear power purchase agreements, a semiconductor customer co-designing proprietary silicon architecture down to the numerics of its matrix engines, a cloud tenant optimizing planet-scale optical network topologies, and an infrastructure planner pouring concrete for advanced computing campuses the size of small towns. The remainder of this paper documents, layer by layer, how completely that collapse has already occurred.

Section 2: The Modern Hardware Landscape: Custom Silicon and Hyper-Scale Clusters

The physical manifestation of One Industrial System is found in the massive capital expenditures pouring into specialized silicon and unprecedented computing campuses. The illusion of a clean, commoditized cloud layer has shattered under the weight of exponential frontier AI scaling laws. AI clusters are no longer standard enterprise server rooms; they are planetary-scale industrial facilities where micro-transistor architectures dictate the thermodynamic layout of the concrete structures housing them. When the first-quarter 2026 earnings season closed, the four largest U.S. hyperscalers had collectively guided to roughly $725 billion in capital expenditure for the year — Amazon at approximately $200 billion, Microsoft near $190 billion for the calendar year, Alphabet at $175–185 billion, and Meta at a raised range of $125–145 billion — with Goldman Sachs now projecting a combined $5.3 trillion of hyperscaler capex between fiscal 2025 and fiscal 2030.[1][2][3] The quarterly cadence tells the same story: Alphabet’s capex more than doubled year-over-year to $35.7 billion in Q1 2026, Amazon’s reached $44.2 billion as AWS grew 28 percent and its in-house chip business hit a $20 billion revenue run rate, and Microsoft’s fiscal-third-quarter capex rose 84 percent to $30.9 billion as its AI business surpassed a $37 billion annual run rate.[5] Analysts warned that free cash flow across the group would compress sharply — with Amazon’s projected to turn negative — a capital-intensity profile that belongs to railroads and utilities, not to the software industry these firms once epitomized.[4][55]

Jefferies analyst Brent Thill, responding to skeptics who saw a bubble in the synchronized spending, was blunt in his dismissal:

“The bear thesis is garbage.”

— Brent Thill, Jefferies, to the Financial Times [2]

Whether or not one shares Thill’s confidence, the sheer physicality of the buildout is no longer in dispute. What follows is a survey of the hardware landscape as it stands in mid-2026, organized around three phenomena: Nvidia’s transformation from chip vendor to system architect, the hyperscalers’ custom-silicon counter-offensive, and the arrival of the gigawatt-scale megaproject.

2.1 Nvidia’s Platformization and the CUDA Moat

At the center of this landscape sits Nvidia, which pioneered the transition from component provider to full-system architect. Nvidia realized early that selling loose GPUs would create a bottleneck at the networking layer: a ten-thousand-GPU training run is only as fast as its slowest collective-communication operation, and the value of the silicon is hostage to the fabric that connects it. Through the strategic assimilation of Mellanox’s InfiniBand networking business and the development of proprietary NVLink topologies, Nvidia achieved system-level domination — it no longer sells chips so much as it sells pre-integrated factories for intelligence.

When an operator deploys the Nvidia Blackwell GB200 NVL72 platform, it is not buying chips; it is buying a fully integrated, liquid-cooled, multi-cabinet supercomputer. Each NVL72 rack fuses 72 Blackwell GPUs and 36 Grace CPUs into a single NVLink domain with roughly 1.8 terabytes per second of bidirectional GPU-to-GPU bandwidth and over 13 terabytes of pooled high-bandwidth memory, so that the entire 1.36-metric-ton, roughly 120-kilowatt rack behaves computationally like one enormous accelerator.[65][66] The consequences ripple downward into the physical world: a rack that draws 120 kilowatts — against a global enterprise average of under 8 kilowatts — cannot be air-cooled, cannot sit on ordinary raised flooring, and cannot be hosted in the majority of data centers built before the current decade.[66] The transistor now dictates the building. This physical architecture is bound tightly to the CUDA software ecosystem, a two-decade accumulation of compilers, kernels, libraries, and developer habits that forces the world’s AI researchers to optimize their algorithms around Nvidia’s hardware layout, and which constitutes one of the deepest competitive moats in industrial history.

The financial results of platformization are without precedent in the semiconductor industry. Nvidia’s fiscal 2026 second quarter delivered $46.7 billion in revenue with $41.1 billion from the data center segment; founder and CEO Jensen Huang framed the moment in explicitly industrial terms:[7]

“Blackwell is the AI platform the world has been waiting for.”

— Jensen Huang, Founder and CEO, Nvidia [7]

By the first quarter of fiscal 2027, reported in the spring of 2026, the company’s quarterly revenue had reached a record $81.6 billion, with data center revenue of $75.2 billion — up 92 percent year over year — and networking revenue alone growing 199 percent to $14.8 billion, driven by the ramp of Blackwell Ultra systems and demand for InfiniBand, Spectrum-X Ethernet, and NVLink.[6] The composition of that revenue is a portrait of the new economy: roughly half from hyperscalers, and the remainder from a widening base of AI clouds, industrial players, enterprises, and — significantly — sovereign customers, foreshadowing the geopolitics examined in Section 4.[6]

2.2 The Hyperscaler Counter-Offensive: Custom Silicon Silos

To escape Nvidia’s high margins and design constraints, the major cloud hyperscalers are aggressively verticalizing their internal hardware stacks through application-specific integrated circuits (ASICs). What began a decade ago as cost-optimization side projects has matured, in 2025–2026, into full frontier-class silicon programs, each fabricated on TSMC’s most advanced nodes and each welded to a proprietary software stack. The strategic logic is identical across all four firms: capture the roughly 70-to-80-percent gross margin that Nvidia extracts from merchant silicon, tailor the numerics of the chip to the exact tensor shapes of the in-house models, and convert hardware lock-in from a liability into a product.[51][53]

Google TPU: A Decade Ahead

Google’s Tensor Processing Unit is the most mature custom AI silicon effort in existence, now in its seventh generation. Ironwood, announced at Cloud Next 2025 and made generally available in late 2025, delivers roughly 4,614 FP8 teraflops per chip with 192 gigabytes of HBM3E, and scales to a 9,216-chip “superpod” delivering 42.5 FP8 exaflops with 1.77 petabytes of aggregate high-bandwidth memory.[50][51][52] Designed with Broadcom on TSMC’s N3P process, Ironwood closes nearly the entire specification gap with Nvidia’s flagship, while Google’s procurement structure yields an all-in total cost of ownership per chip that SemiAnalysis estimates at roughly 44 percent below a comparable GB200 server.[52] Crucially, Google has broken with a decade of internal-only deployment and begun selling TPU systems externally: Anthropic’s October 2025 commitment to up to one million TPUs — the largest deal in Google Cloud history, structured as roughly 400,000 Ironwood units sold directly through Broadcom and 600,000 rented through Google Cloud — converted the TPU from an internal cost advantage into a merchant weapon, and by the spring of 2026 Google had previewed an eighth generation split into a Broadcom-designed training chip and a MediaTek-designed inference chip targeting TSMC’s 2-nanometer node.[49][52] Even Meta, which fields its own accelerator program, entered arrangements to rent TPU capacity for selected inference workloads — perhaps the clearest single signal that the custom-silicon era has arrived.[51]

AWS Trainium: Co-Design as Strategy

Amazon Web Services has pursued the most explicitly co-designed path. Trainium3, launched at re:Invent 2025 as AWS’s first 3-nanometer chip, delivers 2.52 petaflops of FP8 compute per chip with 144 gigabytes of HBM3e at 4.9 terabytes per second of bandwidth; a fully configured Trn3 UltraServer connects 144 chips through the new NeuronSwitch-v1 all-to-all fabric into a 362-petaflop system, and UltraClusters can lash together up to one million Trainium chips in a single flat network domain.[10][11] The chip was developed in close collaboration with Anthropic, whose engineers provided direct input on training speed, inference latency, and energy efficiency, and who write low-level kernels against the silicon itself — a degree of algorithm-hardware fusion that would have been unthinkable in the modular era.[8][77] The design philosophy deliberately privileges hardware density and performance-per-watt over single-chip peak performance: AWS claims 4.4 times the compute and four times the energy efficiency of the prior generation, and cites customers cutting training and inference costs by up to 50 percent relative to GPU alternatives.[10][11] AWS CEO Matt Garman explained the deeper strategic point when describing why the company could ramp Trainium volumes four times faster than any chip it had ever deployed:

“We control the whole process, the whole stack.”

— Matt Garman, CEO, Amazon Web Services [11]

In a notable strategic extension, AWS has begun pushing its silicon beyond its own walls: the AWS “AI Factories” program, announced alongside Trainium3, brings AWS-designed AI infrastructure — including Trainium — into customers’ own data centers, while the forthcoming Trainium4 will support Nvidia’s NVLink Fusion interconnect, enabling heterogeneous clusters that mix Amazon and Nvidia silicon in a single fabric. The cloud giant, in other words, is evolving toward a merchant posture for hardware it once guarded as a purely internal advantage.[64][76]

Meta MTIA and Microsoft Maia: The Inference Flywheel

Meta’s custom program, the Meta Training and Inference Accelerator (MTIA), is designed in collaboration with Broadcom and fabricated on TSMC nodes, and has already been deployed by the hundreds of thousands for inference across Facebook and Instagram. In March 2026 the company disclosed one of the most ambitious silicon roadmaps in the industry — four new MTIA generations for deployment through 2027, culminating in a 2×2-chiplet part scaling to 10 petaflops of FP8 with up to 512 gigabytes of HBM — while simultaneously expanding its Nvidia partnership for “millions” of GPUs, an explicit two-track strategy of merchant training silicon and custom inference silicon.[51] Microsoft, after a delayed start, deployed its Maia 200 accelerator in January 2026 — a TSMC 3-nanometer part with over 140 billion transistors delivering more than 10 petaflops of FP4 — which now serves OpenAI model traffic and Microsoft 365 Copilot workloads.[51] OpenAI itself, in partnership with Broadcom, has pushed its custom inference ASIC through design completion toward volume production on TSMC’s 3-nanometer process in the second half of 2026, targeting deployment across as much as 10 gigawatts of capacity by decade’s end.[62] The pattern is universal: every entity with frontier ambitions is becoming a semiconductor company, and every semiconductor strategy terminates in the same handful of Taiwanese fabs.

| Program / Chip | Design Partners & Process | Primary Strategic Focus |

| Google TPU v7 “Ironwood” (+ v8 split) | Broadcom & MediaTek; TSMC N3P (v8 at 2nm) | 9,216-chip superpods (42.5 EFLOPS); ~44% lower TCO vs. GB200; external sales to Anthropic (~1M chips) and Meta rentals[49][50][52] |

| AWS Trainium3 (+ Trainium4) | Annapurna Labs, co-designed with Anthropic; TSMC 3nm (N3P) | 144-chip UltraServers (362 PFLOPS); 1M-chip UltraClusters; density and perf-per-watt over peak; AI Factories external deployment; NVLink Fusion in Trn4[10][11][64][76] |

| Meta MTIA (gens 300–500) | Broadcom; TSMC advanced nodes | Hundreds of thousands deployed for ranking/recommendation and Llama inference; roadmap to 10 PFLOPS FP8 by 2027; dual-track with Nvidia GPUs[51] |

| Microsoft Maia 200 | In-house; TSMC 3nm, 140B+ transistors | >10 PFLOPS FP4; serves OpenAI and Copilot traffic; “most performant first-party silicon from any hyperscaler” claim[51] |

| OpenAI custom ASIC (with Broadcom) | Broadcom; TSMC 3nm; H2 2026 mass production | Inference-optimized; planned deployment across up to 10 GW of capacity by 2029[62] |

Table 2. The hyperscaler custom-silicon ecosystem, mid-2026. Every program converges on TSMC’s leading-edge nodes and advanced packaging.

The convergence on a single foundry deserves emphasis, because it is the quiet load-bearing fact of the entire industry. TSMC’s first-quarter 2026 revenue reached approximately $35.7–35.9 billion — up more than 35 percent year over year — with gross margin expanding to 66.2 percent, full-year revenue guidance raised above 30 percent growth, and management describing AI demand as “extremely robust” as agentic workloads multiply token consumption; capital expenditure for the year is guided to $52–56 billion, with 70–80 percent devoted to leading-edge nodes.[47][48][84][86] CoWoS advanced packaging — the interposer technology through which nearly every AI accelerator on Earth must physically pass — remains, in the company’s own characterization, extremely tight and effectively sold out, even as capacity scales toward a nearly fourfold expansion.[48][85] The Stanford 2026 AI Index states the strategic exposure plainly: a single Taiwanese company fabricates nearly every leading AI chip, making the entire global AI hardware supply chain dependent on one foundry.[29]

2.3 The Megaproject Era: Gigawatt-Scale Clusters

As software scaling transitions into a race for physical footprint, the scale of data center megaprojects has broken all historical precedents. Consider four flagship projects, each of which would have been the largest computing facility ever constructed had it been announced five years ago, and each of which is now merely one entry in a crowded field.

First, Amazon’s Project Rainier. On 1,200 acres of former farmland in New Carlisle, Indiana, AWS built and activated — in under a year — an $11 billion campus dedicated to a single customer, Anthropic, for training and serving the Claude model family. At activation in October 2025 the site ran nearly 500,000 Trainium2 chips, a figure that crossed one million chips across the Rainier program by year-end; the completed campus is designed for roughly 30 buildings exceeding 200,000 square feet each and a grid draw of about 2.2 gigawatts, which would make it the single largest electricity customer in the 100-plus-year history of its local utility.[8][9][61][63] In November 2025, Amazon announced a further $15 billion Phase 2 expansion across Northwest Indiana, and the commercial architecture around the campus deepened commensurately: Anthropic committed to spend more than $100 billion on AWS compute over ten years and to reserve up to five gigawatts of Trainium capacity, while Amazon expanded its investment in Anthropic by up to an additional $25 billion.[61] Ron Diamant, the AWS distinguished engineer who serves as head architect of Trainium, captured the internal sense of scale:

“Project Rainier is one of AWS’s most ambitious undertakings to date.”

— Ron Diamant, Distinguished Engineer and Head Architect of Trainium, AWS [9]

His colleague Prasad Kalyanaraman, AWS vice president of infrastructure services, articulated the doctrinal lesson — the necessity, in his words, of being able to[8]

“control the stack all the way from the lower layers of the infrastructure.”

— Prasad Kalyanaraman, VP of Infrastructure Services, AWS [8]

Second, Microsoft’s Fairwater campus in Mount Pleasant, Wisconsin. Spanning 315 acres and 1.2 million square feet across three buildings — assembled from 26.5 million pounds of structural steel, 46.6 miles of foundation piles, and 120 miles of medium-voltage cable — Fairwater is engineered not as a collection of servers but as one machine: hundreds of thousands of Nvidia GB200-class GPUs fused into a single flat network, laid out in a two-story configuration to shave nanoseconds of latency between racks, and cooled by a closed-loop liquid system fed by the second-largest water-cooled chiller plant on the planet.[12] The facility went live ahead of schedule in April 2026, with CEO Satya Nadella describing it as[13]

“the world’s most powerful AI datacenter.”

— Satya Nadella, CEO, Microsoft [13]

Microsoft has committed more than $7 billion to the Wisconsin site alone, is constructing identical Fairwater-class facilities elsewhere in the United States, and is extending the pattern internationally through a $6.2 billion Norway deployment and a $30 billion United Kingdom commitment through 2028.[12][79][80]

Third, OpenAI’s Stargate program. Announced at the White House in January 2025 as a $500 billion, 10-gigawatt commitment with Oracle and SoftBank, Stargate expanded within nine months to nearly 7 gigawatts of planned capacity and over $400 billion of committed investment across a flagship campus in Abilene, Texas and new sites in Texas, New Mexico, Ohio, Wisconsin, and beyond — putting the venture ahead of schedule on its full commitment, with the July 2025 Oracle agreement alone covering $300 billion over five years for 4.5 gigawatts of capacity.[14][15][62] Epoch AI’s independent tracking counts more than 9 gigawatts of planned capacity across seven U.S. sites — comparable to the peak power demand of New York City — and notes that at least three sites will sidestep interconnection queues entirely by building on-site natural gas generation, a detail that quietly concedes the thesis of this paper: the AI lab has become its own utility.[16] OpenAI’s chief executive Sam Altman has described total infrastructure commitments of roughly $1.4 trillion over eight years, a sum Nvidia’s Jensen Huang called the largest computing project in history.[17]

Fourth, Meta’s twin superclusters. The company’s Prometheus cluster in New Albany, Ohio — expected online in 2026 at roughly one gigawatt — and its Hyperion campus in Louisiana — a $27 billion joint-venture development beginning at 2 gigawatts and scaling toward 5 gigawatts on 2,250 acres — anchor a fleet that Meta intends to grow beyond 10 gigawatts of total capacity by the end of 2026.[18][54] Mark Zuckerberg has framed the entire program as the physical substrate for delivering, in his words,[5]

“personal superintelligence to billions of people.”

— Mark Zuckerberg, CEO, Meta Platforms [5]

Nor is the club closed: Elon Musk’s xAI announced a $20 billion data center in Southaven, Mississippi — the largest private investment in that state’s history — within a single news cycle of Meta’s energy announcements, a cadence of gigawatt-scale commitments that has become almost routine.[59]

The modern constraint is no longer chip availability but the raw physics of grid delivery. Synergy Research Group counted roughly 1,360 operational hyperscale data centers at the end of 2025 — nearly triple the count of early 2018 — with a known future pipeline of nearly 800 additional facilities whose aggregate capacity exceeds everything currently operating; the firm expects total hyperscale capacity to double in just over twelve quarters and hyperscalers’ share of all data center capacity worldwide to climb from 48 percent today to 67 percent by 2031.[26][27][87] On the demand side, Goldman Sachs Research forecasts that U.S. data center power consumption will more than double from 31 gigawatts in 2025 to 66 gigawatts in 2027 — commanding roughly 8.5 percent of the nation’s total peak summer electricity demand, up from 4.1 percent — on installed capacity reaching approximately 95 gigawatts by the end of 2027.[22] The Department of Energy’s Lawrence Berkeley National Laboratory established the baseline trajectory: data centers consumed about 4.4 percent of total U.S. electricity in 2023 and are projected to consume between 6.7 and 12 percent by 2028, with load growth having tripled over the prior decade.[23][57] The report’s lead researcher, Arman Shehabi, marveled at the discontinuity relative to his own prior surveys:

“There’s so much difference in the industry.”

— Arman Shehabi, Staff Scientist, Lawrence Berkeley National Laboratory [24]

To sustain this growth, technology companies are bypassing traditional utility procurement entirely and reaching directly into the generation layer — above all, into nuclear power. In January 2026, Meta announced agreements with Vistra, TerraPower, and Oklo supporting up to 6.6 gigawatts of new and existing firm nuclear power by 2035 for its Prometheus supercluster: 20-year power purchase agreements with Vistra covering 2,609 megawatts from the Perry, Davis-Besse, and Beaver Valley plants (including the largest corporate-backed nuclear uprates in U.S. history), funding for two TerraPower Natrium units with rights to six more, and a 1.2-gigawatt Oklo advanced-reactor campus in Pike County, Ohio — all layered atop Meta’s earlier 20-year, 1.1-gigawatt Constellation agreement that rescued the Clinton Clean Energy Center from planned closure.[18][19][20][21] TerraPower’s chief executive Chris Levesque framed the industrial timetable candidly:

“We must deploy gigawatts of advanced nuclear energy in the 2030s.”

— Chris Levesque, President and CEO, TerraPower [19]

Meta is not alone. Talen Energy and Amazon expanded their agreement to supply up to 1.9 gigawatts of nuclear power through at least 2042; Microsoft’s 20-year power purchase agreement is financing the restart of Unit 1 at the Crane Clean Energy Center — the former Three Mile Island — as early as 2027; and Holtec’s Palisades plant became the first U.S. commercial reactor to formally return from decommissioning to operational status.[21] Retired reactors resurrected, new reactor classes bankrolled, uprates funded by social-media companies: the energy layer and the intelligence layer have signed their merger papers. Megaclusters are now structurally limited not by algorithmic efficiency, but by the timeline required to pour concrete and connect gigawatt-scale infrastructure directly to nuclear or geothermal baseload. The modern frontier model is no longer code; it is a sprawling industrial monument of silicon, copper, and raw electrical current.

Section 3: The Collapse of the Modular Stack: From Horizontal to Vertical Integration

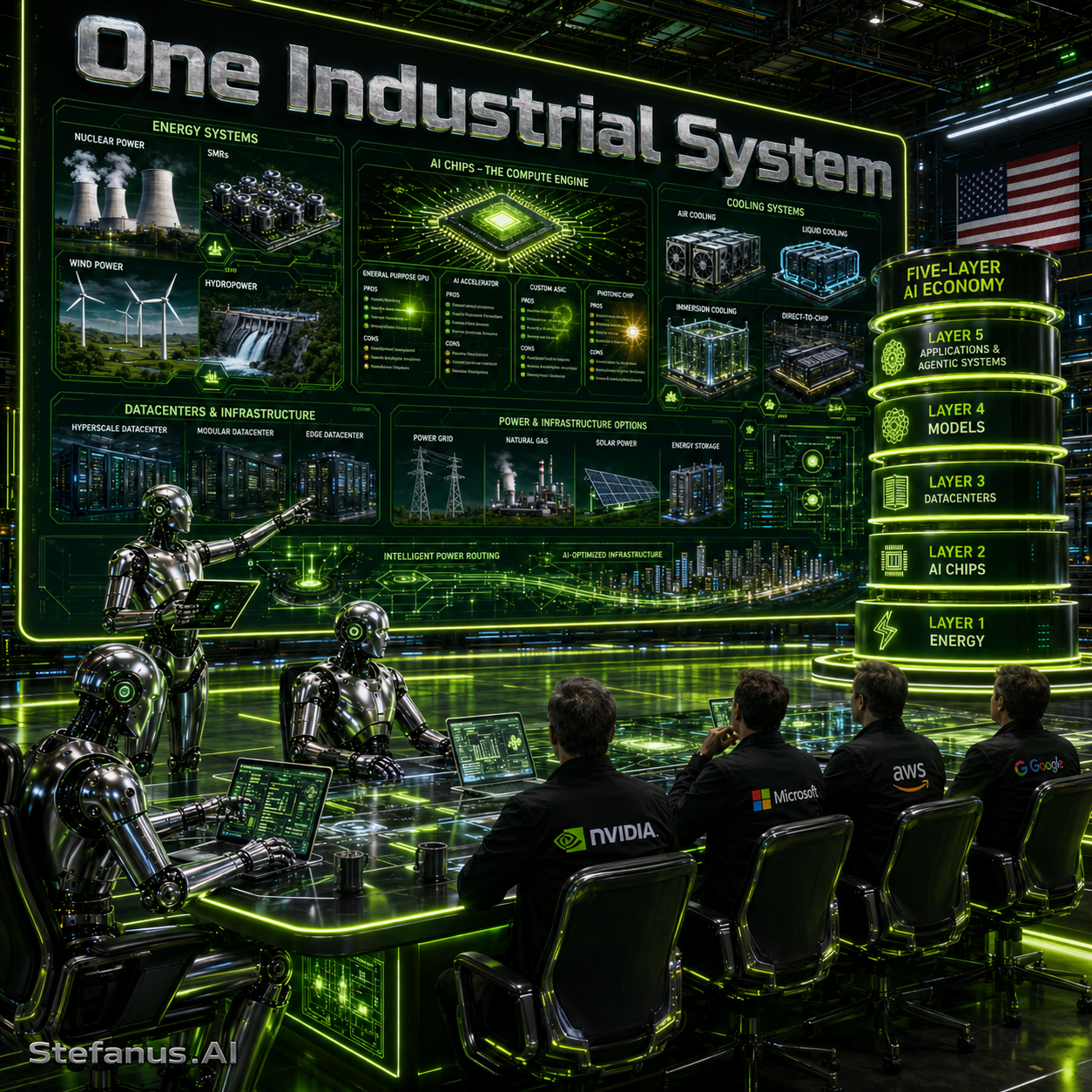

As the massive capital expenditures and hardware footprints detailed in Section 2 demonstrate, the physical scale of modern compute has shattered the illusion of a clean, commoditized cloud layer. The frontier AI cluster is no longer a standard server room running independent software; it is a highly specialized environment where transistor architectures dictate thermodynamic layout, where the memory stack on a single accelerator determines the diameter of the chilled-water pipes in the building, and where the training schedule of a single model family determines the dispatch profile of a nuclear power plant three states away. This intense physical dependency triggers a structural collapse of the traditional modular tech stack, giving rise to what this paper formalizes as the Five-Layer AI Economy.

Under the old modular regime, each layer of the technology stack was a market. Energy was purchased from regulated utilities at posted tariffs. Chips were bought from merchant semiconductor vendors on standard terms. Data center capacity was leased from colocation providers or rented from clouds by the hour. Models were trained by whoever cared to train them, on whatever hardware happened to be available. Applications were built by anyone with an API key. The interfaces between layers were priced, standardized, and — critically — substitutable: a buyer dissatisfied with one supplier could switch to another without redesigning its own product. That substitutability was the entire foundation of the horizontal technology economy, and of the startup ecosystem that flourished within it.

The Five-Layer AI Economy obliterates these boundaries. As scaling laws dictate that capability is directly proportional to industrial throughput, the five distinct layers have collapsed into a single, tightly coupled machine, in which optimization at any one layer is impossible without co-optimization of the layers above and below it. The hierarchy is best visualized as a vertical stack, with economic value flowing upward and physical constraint flowing downward.

| LAYER 5 — APPLICATIONS & AGENTIC SYSTEMS (The Economic Value Engine) |

| LAYER 4 — MODELS (The Software Brains) |

| LAYER 3 — DATACENTERS & INFRASTRUCTURE (The AI Factory) |

| LAYER 2 — AI CHIPS (The Intelligence Engine) |

| LAYER 1 — ENERGY (The Bottom Constraint) |

Figure 1. The Five-Layer AI Economy. Value accrues upward; physical constraint propagates downward. No layer can any longer be optimized, priced, or procured in isolation.

Layer 1: Energy — The Bottom Constraint

At the base of the entire economy sits the physical grid. Every token generated, every weight adjusted, is fundamentally an act of converting raw electricity into managed heat. AI labs can no longer simply draw power from local utilities; training next-generation models requires gigawatt-scale, high-availability baseload power delivered on timelines that ordinary interconnection queues — which now stretch toward 2031 in some U.S. zones — cannot accommodate. This reality has turned AI operators into direct energy buyers, forcing them to negotiate unprecedented power purchase agreements with existing nuclear plants, to bankroll advanced reactor developers years before first criticality, and in some cases to build their own on-site gas generation rather than wait for the grid at all.[16][18][21][22] The macroeconomic signature of the energy layer is already visible in national statistics: Goldman Sachs projects U.S. data center demand doubling to 66 gigawatts by 2027, the Berkeley Lab projects data centers absorbing up to 12 percent of U.S. electricity by 2028, and Harvard’s Belfer Center documents the downstream consequences — from Dominion Energy’s first base-rate increase since 1992 to a July 2024 incident in which sixty Northern Virginia data centers disconnected simultaneously, forcing emergency grid interventions.[22][23][25] Electricity has become the currency in which intelligence is denominated, and access to it has become — as Section 4 will show — a tool of statecraft.

Layer 2: AI Chips — The Intelligence Engine

Directly atop energy sits the microarchitecture that processes it. While general-purpose compute sufficed for the internet era, frontier AI demands specialized parallel processors whose entire design philosophy is thermodynamic: maximize useful floating-point operations extracted per joule delivered from Layer 1. Because merchant silicon carries a heavy margin premium, leading entities are aggressively bypassing market intermediaries. They co-design proprietary ASICs directly with foundries like TSMC — Google with Broadcom and MediaTek, Amazon with Annapurna Labs and Anthropic, Meta with Broadcom, OpenAI with Broadcom — tailoring numerics, memory hierarchies, sparsity engines, and interconnect topologies to their exact algorithmic needs.[49][51][53] The layer’s two chokepoints have become the most strategically watched objects in the world economy: TSMC’s leading-edge fabrication and CoWoS advanced packaging, effectively sold out and running at full utilization; and the high-bandwidth memory oligopoly of SK Hynix, Samsung, and Micron, whose 2026 HBM output was fully reserved under multi-year agreements before the year began, dragging the entire DRAM complex into a shortage that executives warn may persist to 2027 and beyond.[44][45][46][48] When Nvidia’s Jensen Huang was asked at CES 2026 about the memory crunch rippling into consumer electronics, his answer was a précis of the new industrial order:

“Every factory, every HBM supplier, is gearing up.”

— Jensen Huang, Founder and CEO, Nvidia, at CES 2026 [46]

Layer 3: Datacenters and Infrastructure — The AI Factory

Silicon is useless in isolation; it must be orchestrated. Layer 3 transforms loose chips into a unified supercluster — the “AI factory.” This layer covers data center real estate, substations and transmission interconnects, liquid-cooling distribution, and ultra-low-latency network fabrics: custom optical switches, InfiniBand and Spectrum-X topologies, NVLink and NeuronSwitch domains, petabit-scale Elastic Fabric Adapter meshes. The engineering tolerances are unforgiving. If a network fabric experiences even minor packet loss or a single mis-tuned collective operation, thousands of interconnected accelerators stall in synchronized idleness, burning millions of dollars of power and depreciation while producing nothing. Infrastructure planning has therefore become an art of thermodynamic and data-routing orchestration: Microsoft literally stacked Fairwater’s racks in a two-story configuration to shorten cable runs, and AWS treats the entire 1,200-acre New Carlisle campus as a single unit of compute — one vast, tightly networked machine.[12][61] This is also the layer where the industry’s market structure is consolidating fastest: hyperscale operators already control 48 percent of all data center capacity on Earth and are projected to control 67 percent by 2031, an infrastructural enclosure with no precedent in the history of computing.[27]

Layer 4: Models — The Software Brains

Only after the first three physical layers are fully optimized can the foundational model be trained. This layer represents the algorithmic architecture — the large language models, multimodal networks, and complex reasoning engines that constitute the visible face of the AI revolution. In the unified system, the model is no longer written in a vacuum. It is deeply co-designed around the specific constraints of the data center’s network fabric (Layer 3) and the exact tensor shapes, precision formats, and memory bandwidths favored by the underlying silicon (Layer 2). The evidence is concrete: Anthropic engineers write low-level kernels that interface directly with Trainium silicon and contribute to the AWS Neuron software stack; Trainium3’s designers doubled MXFP8 throughput specifically because their anchor customer trains in that format; Google’s Gemini family is architected around the 9,216-chip torus topology of a TPU superpod; and the industry-wide pivot toward reasoning models with enormous inference-time compute has reshaped chip roadmaps — driving the memory-heavy designs of Blackwell Ultra, Ironwood, and Maia 200 — within a single product generation.[52][53][77] The direction of causality has inverted. In the modular era, hardware chased software; in One Industrial System, model architecture and physical plant are drafted at the same table, often literally by the same engineers.

Layer 5: Applications and Agentic Systems — The Economic Value Engine

The apex of the stack is where intelligence is deployed to generate revenue: agentic workflows, autonomous coding systems, enterprise copilots, scientific discovery pipelines, and consumer interfaces. Under the modular myth, any startup could build a great application, because the layers beneath it were commodities available to all comers at identical prices. In the Five-Layer AI Economy, an application’s unit economics and latency are entirely dependent on how tightly it integrates with the underlying layers. Inference now constitutes roughly two-thirds of all AI compute spending, which means an application’s gross margin is a direct function of the cost-per-token of the silicon it runs on — and the cheapest tokens belong to whoever owns the chip, the building, and the power contract beneath it.[51][81] Microsoft’s AI revenue run rate surpassing $37 billion, Amazon’s chip business reaching a $20 billion run rate, Google Cloud’s backlog swelling past $460 billion, and Anthropic’s run-rate revenue climbing past $30 billion are not five separate business stories; they are one story — the monetization layer of a single vertically integrated machine, pulling value all the way down from the power plant.[5][49] The Stanford AI Index adds the demand-side corroboration: U.S. consumer surplus from generative AI reached an estimated $172 billion annually by early 2026, with the median value per user tripling in a single year, even as productivity gains of 14–73 percent in structured work began visibly reshaping early-career employment.[28][88]

3.1 The Interdependency Trap

This hierarchical stack is not merely a conceptual model; it is a web of tight operational dependencies in which a failure at the basal energy layer instantly degrades performance at the application apex. A transformer delivery delayed by a 128-week lead time postpones a substation; the postponed substation strands a building of installed accelerators; the stranded accelerators delay a training run; the delayed training run pushes back a model release; the missed model release cedes application-layer market share that may never be recovered. Conversely, a breakthrough at the model layer — say, a reasoning architecture that multiplies inference-time compute per query — cascades downward as an unplanned demand shock on memory supply, packaging capacity, and regional grids. The layers can no longer be decoupled on the open market without introducing severe latency, cost, and execution risk, because the market interfaces that once connected them — spot GPU rental, standard colocation leases, utility tariffs — are either sold out for years or priced at panic levels: DRAM contract prices rose roughly 90 percent in a single quarter, HBM is sold out through 2026 under multi-year reservations, Blackwell lead times run six to twelve months, and CoWoS packaging is spoken for through 2028.[44][45][46][48][65][85]

It is precisely this trap that forces leading AI firms to abandon horizontal specialization entirely. To survive, the modern AI lab must reject the open market and absorb a complex, four-fold industrial identity within a single corporate entity:

1. An Energy Buyer securing sovereign-scale power — negotiating twenty-year nuclear power purchase agreements, funding reactor uprates and restarts, and in extremis building generation behind its own meter.[18][19][21]

2. A Semiconductor Customer dictating foundry tape-outs — co-designing ASICs with Broadcom, MediaTek, and Annapurna, reserving TSMC leading-edge wafers and CoWoS slots years in advance, and locking down multi-year HBM supply agreements.[48][51][53]

3. A Cloud Tenant (and increasingly a Cloud Architect) engineering planetary networks — negotiating gigawatt-scale, multi-year capacity deals across multiple providers, and co-designing the fabric topologies its models will train on.[8][49][61]

4. An Infrastructure Planner pouring concrete for the next generation of industrial mills — siting campuses against water, land, fiber, and grid maps; managing thousands of construction workers; and navigating local zoning politics from Indiana to Louisiana.[12][54][61]

When these four identities merge, the technology stack ceases to be a collection of isolated commercial products and transforms into One Industrial System. This absolute vertical integration does not merely rewrite corporate strategy; it fundamentally reorders the global geopolitical landscape, driving the sovereign infrastructure races analyzed in the following section.

Section 4: Macro Implications: Geopolitics, Startups, and National Policy

The transition from modular software to a unified industrial stack has fundamentally altered the geopolitical chessboard. Computing power is no longer merely a commercial asset; it is a metric of national power akin to steel production in the twentieth century or naval tonnage in the nineteenth. The Center for a New American Security’s Sovereign AI Index quantifies the starting distribution bluntly: the United States and China together control roughly 90 percent of the computing power needed to develop and deploy frontier AI, with the U.S. hosting more than 5,400 data centers — over ten times any other country — and 55 percent of worldwide hyperscale capacity.[26][29][37] This reality has ignited the global “Sovereign AI” race: a scramble by nation-states to secure every layer of the Five-Layer AI Economy within their geographic or diplomatic borders. The World Economic Forum, in its January 2026 report on the subject, defines the ambition precisely — the ability of economies to shape, deploy, and govern AI ecosystems in accordance with their own values while ensuring strategic and operational control — and observes that several economies are now attempting to own the entire AI value chain, from raw inputs upward.[36]

Historically, nations could participate in the technology economy by specializing in a single horizontal layer — Israel in chip design, Taiwan in advanced fabrication, South Korea in memory, India in software services, the United States in platform architecture. The emergence of One Industrial System renders this distributed model strategically fragile. Because a bottleneck at any single layer halts the entire intelligence pipeline, great powers can no longer entrust their AI trajectories to cross-border, just-in-time supply chains; and middle powers, as Chatham House documents, increasingly regard reliance on foreign cloud and AI providers as a legal and jurisdictional risk in its own right — citing everything from the extraterritorial reach of the U.S. CLOUD Act to the European Commission’s late-2025 market investigations into Amazon’s and Microsoft’s cloud practices.[38] Consequently, national policy is pivoting toward radical industrial statecraft across three fronts.

4.1 The Energy-Compute Nexus

Governments are intervening directly in energy markets, fast-tracking regulatory approvals for nuclear restarts, reclassifying data centers as strategic infrastructure, and dedicating grid expansions to AI campuses. The United Kingdom now allows data centers to apply for “national importance” status that overrides local planning objections; France is drafting legislation to classify data centers as projects of major national interest, cutting approval timelines nearly in half, while state utility EDF has pre-identified reactor-adjacent sites offering two gigawatts for data center development.[39][75] In the United States, the White House’s July 2025 AI Action Plan made “Building American AI Infrastructure” one of its three formal pillars, and the resulting executive actions — more than ninety of them in motion by early 2026 — treat electrons for AI as a national security input.[41][82] Access to the electrical grid is now a tool of statecraft, and the queue position of a substation has become a matter of foreign policy.

4.2 Sovereign Megaclusters

Nation-states are funding domestic hyper-clusters to escape dependence on foreign cloud monopolies. France’s program is the most ambitious in Europe: President Emmanuel Macron announced €109 billion in AI infrastructure investment, anchored by a €10 billion, one-gigawatt decarbonized supercomputer hosting up to 500,000 next-generation chips, and framed the effort in unmistakably political vocabulary:[39]

“This is our fight for sovereignty, for strategic autonomy.”

— Emmanuel Macron, President of the French Republic [39]

The European Union has mobilized €20 billion for its AI Gigafactory program — publicly anchored, sovereignty-first facilities of roughly 100,000 AI chips each, formally written into the EuroHPC regulation in January 2026 — while Mistral AI secured €830 million in institutional debt from a banking consortium to build its own data center near Paris, a financing structure (infrastructure debt, not venture equity) that itself signals the industrialization of the model layer.[40][69] Canada pledged $925.6 million for large-scale sovereign public AI infrastructure and partnered with Telus on a British Columbia compute buildout scaling to 60,000 GPUs; Japan committed public capital to a national AI infrastructure initiative; and the Gulf states moved fastest and at the largest scale, with the UAE’s Stargate campus — a joint venture of G42, OpenAI, Oracle, Nvidia, Cisco, and SoftBank — opening in 2026 and sovereign wealth vehicles across the region treating compute as a reserve asset class.[40][67][68] Across Europe, the Middle East, and Asia, the common mandate is the same: sovereign data must be processed on domestically governed silicon, powered by domestic grids, and managed by domestically accountable entities.

4.3 Export Restrictions and Choke Points

The weaponization of semiconductor manufacturing equipment and advanced chips has formalized a new era of technological containment — and, in 2025–2026, an era of technological deal-making layered on top of it. The trajectory of U.S. policy illustrates how central the chip layer has become to grand strategy. The Biden administration’s January 2025 “AI Diffusion Rule” attempted to regulate the global flow of AI compute through a three-tier country system and even created a new export-control classification for AI model weights themselves; the incoming Trump administration rescinded the rule in May 2025 as innovation-stifling, then substituted its own architecture: the July 2025 AI Action Plan’s “full-stack AI export packages” promoting allied adoption of the entire American system — hardware, cloud, models, and applications bundled together — paired with location-verification requirements on advanced chips and expanded end-use monitoring.[41][42][43] In December 2025 the administration authorized case-by-case sales of H200-class chips to approved Chinese customers in exchange for a 25 percent revenue share, formalized through a January 2026 Bureau of Industry and Security rule and a companion Section 232 tariff proclamation — an arrangement critics in both parties assailed, with former Deputy National Security Advisor Matt Pottinger urging that:[42][83]

“Congress needs to step in, reverse the policy, and put durable guardrails in place.”

— Matt Pottinger, former U.S. Deputy National Security Advisor [42]

Congress, for its part, advanced the AI OVERWATCH Act through the House Foreign Affairs Committee in January 2026 with near-unanimous bipartisanship, proposing to treat advanced-semiconductor exports like weapons sales and to bar Blackwell-class chips from entities of concern.[82] Whatever the eventual equilibrium, the deeper lesson is structural: when the technology stack collapses into one industrial system, export policy at the chip layer becomes de facto policy over every layer above it — over which nations may train frontier models, deploy agentic systems, and ultimately field AI-enabled economies and militaries. Note, meanwhile, what the policy machinery has quietly conceded about the private actors it regulates: the U.S. government now negotiates chip flows with Nvidia the way it once negotiated oil quotas with OPEC members, because a single company’s product roadmap is understood to be a strategic variable in the international system.

4.4 The Startup Squeeze and the New Vassalage

This environment creates an existential crisis for early-stage startups. In a modular ecosystem, a startup with superior algorithms could out-compete an incumbent, because the capital layers of the stack were rentable at marginal cost. In the Five-Layer AI Economy, capital expenditure dictates capabilities, and the minimum viable scale of frontier participation is measured in gigawatts and tens of billions of dollars. The Stanford 2026 AI Index documents the result: over 90 percent of notable AI models in 2025 originated in industry, with academia — the historical seedbed of the field — reduced to a rounding error, and even well-funded challengers structurally dependent on the infrastructure of the giants they nominally compete against.[28][58] The dependency takes intricate forms. OpenAI’s March 2026 funding round drew $50 billion from Amazon, $30 billion from Nvidia, and $30 billion from SoftBank — its suppliers and landlords are now also its shareholders.[62] Anthropic’s compute strategy spans more than one million Amazon Trainium chips, up to one million Google TPUs, and Nvidia GPUs — a sophisticated multi-vendor hedge, but one whose every leg runs through a hyperscaler’s balance sheet.[49][61] New clouds such as CoreWeave raise billions in private debt collateralized by the very Nvidia hardware they deploy for OpenAI, while Nvidia itself invests up to $100 billion into OpenAI, which purchases Nvidia systems — circular capital flows that would be unremarkable inside a single vertically integrated firm and are becoming unremarkable across the industry precisely because the industry increasingly behaves like a single firm.[17] Startups below the frontier are forced into vassalage: trading equity, exclusivity, or data for access to the vertically integrated clusters of technology giants, and building their applications atop APIs whose pricing, latency, and continued existence they do not control. National policy must therefore grapple with a profound dilemma: how to foster domestic innovation when the barrier to entry requires sovereign-scale industrial infrastructure — a question to which, as Section 5 argues, no existing antitrust or industrial-policy framework yet has an answer.

Section 5: The Double-Edged Sword: Resilience vs. Monopoly Risk

The consolidation of the Five-Layer AI Economy into unified corporate systems represents a profound structural shift whose welfare consequences are genuinely ambiguous. Vertical integration is a double-edged sword: it yields unprecedented operational resilience and engineering efficiency, while simultaneously threatening to create the most insurmountable monopolies in economic history. Any honest analysis must hold both edges in view at once, because the same mechanisms that produce the benefits produce the dangers — they are not separable features but two descriptions of a single fact: the concentration of the full production function of intelligence inside a handful of private balance sheets.

| Systemic Resilience (the case for) | Monopoly Risk (the case against) |

| Insulated supply chains: owned silicon, contracted power, self-built campuses buffer merchant shocks[8][18][53] | Insurmountable moats: frontier entry now requires gigawatts and tens of billions in physical capital[1][28] |

| Co-designed efficiency: chip, cooling, network, and model tuned as one machine (e.g., ~44% TCO advantage of integrated TPU systems)[52][77] | Choked innovation: >90% of notable models from industry; academia and open research priced out of the frontier[28][58] |

| Bottleneck protection: multi-year HBM, wafer, and packaging reservations secure the pipeline[44][48] | Infrastructure monopsony: a few buyers dictate terms to memory makers, foundries, and utilities — and starve everyone else[44][46][72] |

| End-to-end telemetry and fault tolerance: workloads reroute around failures across the whole stack[9][12] | Concentration of epistemic power: a corporate oligopoly controls the infrastructure of knowledge, labor automation, and public discourse[31][32] |

| Speed of execution: cornfield to operating gigawatt campus in under a year[8][9] | Systemic single point of failure: correlated capex, circular financing, and shared downside across the entire economy[17][55] |

Table 3. The vertical-integration balance: the identical structural facts, read as strength and as threat.

5.1 Systemic Resilience

From an engineering and operational standpoint, total vertical control provides massive defense against external shock. By controlling every variable from the basal energy layer to the end-user application, integrated firms insulate themselves from the market volatility that would cripple a modular competitor. Consider supply-chain insulation: a firm that designs its own silicon, secures twenty-year nuclear power purchase agreements, and builds its own campuses is largely immune to merchant chip shortages, spot-market memory panics, and local utility rate spikes — the very disruptions that, in 2026, are savaging every buyer outside the integrated core, as DRAM contract prices surge 90 percent in a quarter and mid-market firms compete for residual capacity after the hyperscalers’ long-term reservations are filled.[44][71][73] Consider co-designed efficiency: thermodynamic and computational gains are unlocked when engineers can modify a neural network’s kernel code to match the exact cooling constraints of the building and the exact systolic-array geometry of the silicon — the source of Google’s estimated 44 percent total-cost-of-ownership advantage per TPU versus merchant GPU servers, of Trainium3’s doubled MXFP8 throughput within an unchanged power budget, and of the reported 50 percent training-cost reductions among AWS’s co-design customers.[10][52][53] And consider fault tolerance: when a single entity manages the entire stack, it can build end-to-end telemetry so that a failed chip deep within a supercluster triggers instant workload rerouting at the model or application layer, minimizing the multi-million-dollar cost of synchronized idleness. The speed dividend is equally real: Amazon took Project Rainier from announcement to full operation — half a million custom chips across a campus the size of a town — in under twelve months, a tempo of industrial execution with few peers in any sector, and one available only to an organization that answers to no external supplier for any critical input.[8][9]

5.2 Monopoly Risk

Conversely, this integration creates an economic moat so wide that traditional antitrust frameworks are rendered nearly obsolete, because the classical tests — consumer price harm, horizontal market share — were never designed for an entity that owns the reactor, the chip, the building, the model, and the marketplace simultaneously. Three compounding dangers stand out.

The Capital Barrier. When the minimum baseline to train a frontier model requires tens of billions of dollars in physical infrastructure — and when Goldman Sachs projects $5.3 trillion of hyperscaler capex through 2030 — market entry becomes impossible for everyone except a few technology giants and well-funded nation-states.[3] This effectively chokes open-source innovation and independent research: the Stanford AI Index’s finding that over 90 percent of notable models now come from industry is not a snapshot of temporary imbalance but the equilibrium of a market whose fixed costs have been raised beyond civil society’s reach, even as the Foundation Model Transparency Index records transparency scores falling from 58 to 40.[28][58]

Infrastructure Monopsony. Because integrated firms act as the primary buyers of energy, memory, and advanced silicon, they dictate terms to power utilities and semiconductor suppliers — and, mechanically, starve potential competitors of vital resources. The 2026 memory market is the textbook case: with hyperscalers reserving HBM and DRAM supply years ahead under multi-year commitments, the three memory makers reallocated wafer capacity toward the highest bidder, consumer and enterprise DRAM prices spiked as much as 90 percent in a quarter, and by June 2026 the reallocation itself had drawn a Sherman Act class action alleging that the coordinated pivot functioned as supply restriction — a dispute whose merits courts will decide, but whose existence demonstrates that the buying power of the integrated core now shapes prices for every computer user on Earth.[44][72][74][75] The same monopsony logic operates at the grid: residential and industrial ratepayers in data center regions are already absorbing rate increases driven by loads they neither requested nor benefit from directly.[25]

The Chokehold on Truth. When the infrastructure of intelligence is concentrated in a tiny corporate oligopoly, those few firms hold structural power over the dissemination of knowledge, the automation of labor, and the digital foundations of modern society. No scholar has pressed this point more insistently than MIT Institute Professor and 2024 Nobel laureate Daron Acemoglu, whose lifetime of work on technology and institutions — culminating in Power and Progress, co-authored with Simon Johnson — argues that whether a transformative technology produces shared prosperity or extraction depends on who controls its direction.[30][32] His diagnosis of the present configuration is unambiguous:

“AI is very much concentrated in the hands of a few people and a few companies.”

— Daron Acemoglu, Institute Professor, MIT; 2024 Nobel Laureate in Economics [32]

In Acemoglu’s framework, today’s integrated hyperscalers fit the “extractive” institutional mold — concentrated ownership, regulatory capture, and business models that extract data and attention at scale — and he has argued through 2026 that public discourse fixates on the wrong questions, urging attention instead to what he calls the “enormous increase” in corporate power and monopoly that the buildout entails.[31] He couples this with a bracing empirical skepticism: his published estimates project AI adding only on the order of 1 to 1.6 percent to GDP over a decade, with roughly 0.55 percent in total-factor-productivity gains — figures that, if even approximately right, imply the $725-billion-per-year industrial machine is being financed against expectations it may not meet, converting monopoly risk and financial-stability risk into the same risk.[30][31][60] The IMF has modeled precisely this contingency: an “AI disappoints” scenario in which weaker productivity gains, lower AI investment, and a market correction reduce global output by roughly 1.2 percent within a couple of years — a reminder that when four firms build the same bet simultaneously, they also share the same downside, and so does everyone connected to them.[35][55][70]

Acemoglu is also alert to a subtler channel of concentrated power: the AI laboratories’ race to hire prominent economists in-house — OpenAI’s recruitment of a chief economist and partnership with Harvard’s Jason Furman, Anthropic’s economic advisory council, Google DeepMind’s director of AGI economics — which he worries could tilt the very research base on which policy depends toward the narratives of the firms with the most to gain.[60] When one industrial system supplies the compute, the models, the applications, and increasingly the expert analysis of its own effects, the feedback loops that democracies rely upon to correct concentrated power begin to run through the concentrated power itself.

The ultimate risk of One Industrial System, then, is the total convergence of economic, computational, and political power into a few black-box infrastructures — a systemic single point of failure for the global economy, and a standing constitutional question for every society that depends on it. The resilience documented in Section 5.1 and the risk documented here are not alternatives between which policy can choose; they arrive together, welded to the same machine. The task of the coming decade is to preserve the first while disciplining the second — through interoperability mandates, compute-access programs for research and startups, transparency requirements, structural separation where feasible, and the sovereign public infrastructure investments surveyed in Section 4 — before the machine’s owners become, by default, the governors of everything built upon it.

Section 6: Strategic Pillars of the Five-Layer AI Economy

To operationalize the core insights of this paper, this section distills seven strategic pillars that define survival and dominance within the new industrial paradigm. Each pillar pairs a structural insight — a fact about how the fused stack now behaves — with the strategic action it compels. Together they constitute a field manual for any organization, or any nation, that intends to remain a principal rather than a vassal in the Five-Layer AI Economy.

Pillar 1: The Frontier Model as an Industrial Supply Chain

Insight: Software scaling laws have transformed into physical supply-chain scaling laws. The Kaplan power laws that once described the relationship between compute and capability now describe, transitively, the relationship between concrete, copper, uranium, and capability.[56]

Action: Success is no longer determined by algorithmic breakthroughs alone, but by the continuous, unbroken orchestration of land, concrete, copper, silicon, and code. Organizations must build supply-chain intelligence functions of industrial caliber — tracking transformer lead times, wafer starts, HBM stack yields, and interconnection queues with the same rigor they apply to loss curves — because in the fused stack, a logistics failure is a research failure.

Pillar 2: Chip Access and Cloud Control

Insight: Securing cutting-edge silicon allocation and hyper-scale data center capacity is the minimum baseline for frontier entry, and merchant availability can no longer be assumed: Blackwell-class systems carry six-to-twelve-month lead times, and TSMC’s leading-edge capacity is effectively spoken for years out.[47][65][85]

Action: Firms must secure priority foundry access or design proprietary ASICs to bypass the margins and supply constraints of merchant silicon — following the paths blazed by Google’s decade-long TPU program, Amazon’s Anthropic-co-designed Trainium, Meta’s Broadcom-designed MTIA, and OpenAI’s Broadcom partnership — while hedging across multiple compute suppliers, as Anthropic’s deliberate three-legged strategy (Trainium, TPU, Nvidia) demonstrates.[49][51][61]

Pillar 3: The Co-Designed Model Roadmap

Insight: Model architectures are strictly constrained and shaped by the underlying physical hardware topology — by scale-up domain sizes, memory bandwidth per accelerator, collective-communication latencies, and the precision formats the silicon natively accelerates.[52][53]

Action: AI researchers can no longer build models in isolation; algorithms must be written to exploit the specific memory bandwidth, interconnect speeds, and tensor dimensions of the proprietary cluster, and — in the strongest form of the strategy — the next chip generation must be specified jointly with the next model generation, as Anthropic’s kernel-level collaboration on Trainium3 and Google’s Gemini-TPU co-evolution exemplify. Organizations should staff a dedicated hardware-software co-design function at the same reporting level as model research itself.[77][78]

Pillar 4: Power Procurement and Memory Supply

Insight: Energy-grid integration and high-bandwidth memory allocation are the definitive bottlenecks of AI growth. U.S. data center power demand is set to more than double to 66 gigawatts by 2027, while the world’s entire 2026 HBM output was sold out before the year began and memory executives warn of shortages persisting beyond 2027.[22][44][45]

Action: Leading operators must pivot from technology companies into quasi-industrial utilities — forming direct, decades-long partnerships with nuclear providers as Meta (6.6 GW), Amazon (1.9 GW with Talen), and Microsoft (the Crane restart) have done, pursuing on-site generation where queues bind, and locking down long-term wafer and advanced-packaging supply agreements for memory years ahead of deployment.[16][18][21]

Pillar 5: Infrastructure Finance

Insight: Frontier AI development requires sovereign-scale capital deployment — $725 billion of hyperscaler capex in 2026 alone, trillions across the decade — that traditional venture equity cannot and should not carry, and that is already compressing free cash flow at even the largest firms.[1][3][4]

Action: The industry must shift toward asset-backed project finance, infrastructure bonds, joint-venture structures, and sovereign-wealth consortiums to fund multi-billion-dollar computing facilities — the pattern already visible in Meta’s Blue Owl joint venture for Hyperion, Mistral’s €830 million bank-syndicated data center debt, CoreWeave’s hardware-collateralized private credit, and the SoftBank-Oracle-OpenAI Stargate vehicle — while regulators and investors develop the analytic tools to see through increasingly circular capital flows among chipmakers, clouds, and labs.[14][17][54][69]

Pillar 6: Sovereign Positioning and Policy Fluency

Insight: The state has entered the stack. Export controls, revenue-share arrangements on chip sales, tariffs, sovereign compute programs, and “full-stack” technology diplomacy now determine which layers a firm may access in which jurisdictions — and government demand (sovereign customers already constitute a visible share of Nvidia’s data center revenue) is becoming a first-order market in its own right.[6][41][42]

Action: Firms must treat policy engagement as an operating function, not a lobbying afterthought: architecting deployments for data-sovereignty compliance, qualifying for national programs from the EU’s AI Gigafactories to Gulf sovereign platforms, and building the compliance machinery — location verification, end-use monitoring, diversion controls — that the new export regime demands. Nations, symmetrically, must decide which layers of the stack they will own, which they will ally for, and which dependencies they will consciously accept.[36][37][40]

Pillar 7: Legitimacy, Talent, and the Social License to Build

Insight: The binding constraint of the late 2020s may be neither silicon nor electrons but consent. Zoning boards in Indiana have already forced route changes in multi-billion-dollar expansions; ratepayer backlash is reshaping tariff design in Virginia and Ohio; a class action now targets the memory industry’s reallocation; and public skepticism — fed by employment anxieties the Stanford AI Index shows are no longer hypothetical, with employment among the youngest software developers falling nearly 20 percent even as older cohorts grew — is hardening into the political raw material of the next regulatory wave.[25][28][74][88][89]

Action: Operators must earn a durable social license: prepaying grid infrastructure so residents’ rates do not rise (as Microsoft has in Wisconsin), building closed-loop cooling that retires water objections, funding workforce academies and community benefit agreements, and — hardest of all — demonstrating that the application layer delivers broadly shared value commensurate with the resources the lower layers consume. Acemoglu’s challenge, that technology yields shared prosperity only when institutions and countervailing power force it to, should be read by the industry not as an attack but as the design specification for its own long-term survival.[30][32][79]

Conclusion: The Architecture of the Singular Machine

The transition of artificial intelligence from a mathematical curiosity into a planetary infrastructure project marks the definitive end of the software-exclusive era. For decades, the technology sector operated on the comforting myth of modularity. It assumed that intelligence could be treated as an ethereal layer of code, floating cleanly above the messy, material realities of silicon manufacturing, concrete data centers, and electrical grids. The emergence of the Five-Layer AI Economy has permanently shattered that boundary. The evidence assembled in this paper — $725 billion of synchronized annual capital expenditure, one-million-chip custom-silicon campuses raised on cornfields in under a year, twenty-year nuclear contracts signed by social-media companies, a national grid re-planned around token generation, memory supply sold out for years, and a geopolitics reorganized around wafer allocations — does not describe an industry adopting a new technology. It describes a civilization constructing a new industrial base.

We chose the title “One Industrial System” because it captures the fundamental structural truth of our era: the stack has collapsed. Just as Francis Cabot Lowell’s integrated textile mill combined disparate cottage industries into a single water-powered factory floor, the modern frontier AI enterprise has pulled energy grids, custom semiconductor foundries, hyper-scale optical fabrics, foundational algorithms, and application marketplaces into a single, breathing machine. To analyze a frontier model today by looking only at its weights or its training data is as incomplete as analyzing a nineteenth-century textile mill by looking only at a single thread of cotton. The code is bound to the chip; the chip is bound to the cooling system; the cooling system is bound to the nuclear reactor. They are no longer separate industries interacting through an open market. They are the tightly coupled organs of a single, integrated industrial apparatus.

This paper has also insisted that the machine’s magnificence and its menace are the same property viewed from different angles. The vertical integration that lets a training run reroute around a failed chip in milliseconds is the same integration that raises the price of frontier entry beyond the reach of universities, startups, and most nations. The co-design that extracts forty-four percent more intelligence per dollar is the same co-design that welds every developer to a proprietary stack. The buying power that secures memory for the mission is the same buying power that empties the shelves for everyone else. Lowell’s mills, it is worth remembering, delivered both edges of their own sword: they made cloth astonishingly cheap and abundant, and they also concentrated economic power so completely that the century after them was consumed by the political struggle to discipline it. There is no reason to expect the mills of intelligence to be different, and every reason to begin the disciplining early — through sovereign public compute, interoperability, transparency, and the deliberate cultivation of countervailing power — while the concrete is still wet.